Short Answer

Definition of Economic Bubbles and Anti-Bubbles

In economic discourse, the term “bubble” describes a scenario where asset prices escalate rapidly beyond their intrinsic worth, driven largely by speculative enthusiasm, before eventually collapsing. Contrasting this, the concept of “anti-bubbles” refers to prolonged periods during which markets undervalue assets, leading to sustained declines and pessimism. Both phenomena reflect deviations from fundamental valuations but manifest in opposite directions-bubbles through overvaluation and anti-bubbles through undervaluation.

- Bubble:

A market condition marked by excessive speculation causing asset prices to inflate unsustainably. - Anti-Bubble:

A market phase characterized by persistent undervaluation and declining investor confidence, resulting in prolonged downturns.

Understanding Traditional Bubbles

Bubbles typically arise in environments where investor psychology overrides rational assessment of asset values. This speculative fervor inflates prices beyond sustainable levels, much like how materials undergo phase transitions when exposed to external stimuli such as heat. In this analogy, a stable market equilibrium resembles a solid state, while the speculative bubble represents a volatile, less stable phase. The eventual bursting of a bubble mirrors the abrupt transformation of a material losing its structural integrity.

Conceptualizing Anti-Bubbles

Anti-bubbles invert the traditional bubble dynamic by reflecting a market’s systematic underestimation of asset worth. Instead of exuberance, these periods are marked by waning confidence, disinvestment, and uncertainty. This leads to a self-reinforcing cycle of pessimism, where declining valuations prompt further capital withdrawal, exacerbating the downturn. Understanding anti-bubbles challenges conventional views on market stability and fragility, inviting a reassessment of how prolonged negative sentiment impacts economic systems.

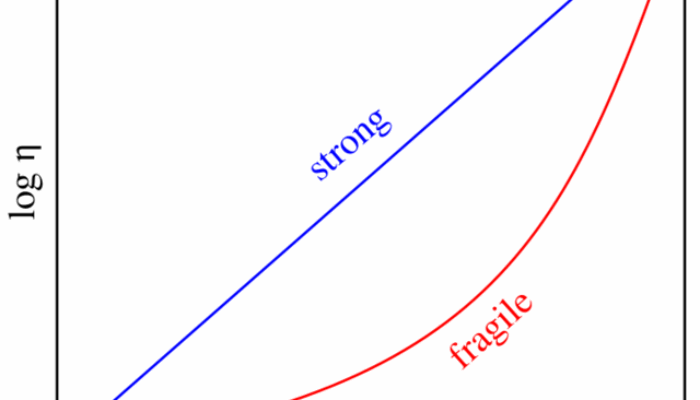

Fragility in Economic Systems: A Physics Perspective

The notion of fragility, originally rooted in materials science, describes how certain substances respond variably to stress-some shatter easily while others deform without breaking. Translating this to economics, markets and economies can be viewed as systems with differing degrees of resilience. Fragile economies, like brittle materials, are prone to collapse under external shocks, whereas more elastic economies absorb stress and adapt without systemic failure.

- Brittle Systems:

Economies or markets that break down abruptly when faced with shocks. - Ductile Systems:

Economies that flex and adjust under pressure, avoiding catastrophic failure.

Mechanisms Behind Anti-Bubble Fragility

Anti-bubbles generate unique vulnerabilities within markets. As investor disenchantment grows, misjudgments about asset fundamentals create a feedback loop of declining confidence and capital flight. This dynamic increases systemic fragility, potentially triggering cascading failures across interconnected financial sectors. The analogy to fragile materials is apt: just as a glass structure can shatter into countless fragments, economies experiencing anti-bubbles risk widespread instability and collapse.

Modeling Anti-Bubbles: Integrating Physics and Economics

Incorporating principles from physics, particularly the study of fragility and volatility, offers a promising avenue for modeling anti-bubbles. By analyzing how markets respond to stress and uncertainty, economists can develop more nuanced frameworks that capture the complex interplay between investor sentiment and asset valuation. This interdisciplinary approach may enhance predictive capabilities, allowing policymakers to identify early warning signs of prolonged downturns and implement measures to stabilize markets.

Measuring and Identifying Anti-Bubbles

Quantifying anti-bubbles poses significant challenges due to the subtlety of their dynamics compared to typical market corrections. One potential method involves tracking the divergence between asset prices and fundamental indicators over time. Persistent undervaluation despite strong fundamentals may signal the presence of an anti-bubble. Developing robust metrics to capture this divergence is crucial for distinguishing anti-bubbles from normal market fluctuations.

Behavioral Foundations and Market Psychology

Anti-bubbles highlight the critical role of investor psychology in shaping market outcomes. As sentiment shifts away from rational expectations toward increased uncertainty and pessimism, market predictability diminishes, resembling a state of entropy. This psychological complexity amplifies perceptions of fragility, similar to how materials near their yield point become more susceptible to failure. Understanding these microfoundations is essential for constructing economic models that reflect real-world investor behavior.

Implications for Economic Theory and Policy

Exploring anti-bubbles through the lens of physical fragility prompts profound questions about economic resilience and stability. Recognizing markets as inherently fragile systems influenced by human psychology encourages the development of adaptive, anticipatory models. Policymakers equipped with insights from this interdisciplinary perspective can better design interventions to mitigate downturns, foster confidence, and promote sustainable growth.

Real-World Examples of Bubbles and Anti-Bubbles

Historical market events illustrate the contrasting dynamics of bubbles and anti-bubbles:

- Dot-com Bubble (Late 1990s):

Characterized by speculative investment in internet companies, leading to inflated valuations and a subsequent crash. - Japanese Asset Price Deflation (1990s-2000s):

An example of an anti-bubble where prolonged undervaluation and economic stagnation followed the burst of a real estate and stock market bubble.

Common Misconceptions About Bubbles and Anti-Bubbles

Bubbles only involve irrational exuberance.

While speculation is central, bubbles also reflect complex interactions between psychology, fundamentals, and market structure.

Anti-bubbles are simply market corrections.

Anti-bubbles represent extended periods of undervaluation and pessimism, distinct from short-term corrections.

Why Understanding Anti-Bubbles Is Crucial

Grasping the dynamics of anti-bubbles enriches economic theory by integrating behavioral insights with physical principles of fragility. This fusion enhances our ability to anticipate market vulnerabilities and design policies that strengthen economic resilience. Ultimately, it contributes to more robust financial systems capable of withstanding shocks and sustaining long-term growth.

FAQ

What are the implications of anti-bubbles for economic policy?

Understanding anti-bubbles allows policymakers to design better interventions to stabilize markets and promote sustainable growth.

Leave a Reply